We’re on a mission to help every Indian understand what a credit score means and how to improve it.

By empowering people with knowledge and tools, we’re building a financially confident India.

Knowledge Partner

1min

1min Loan rejection is not a permanent sentence. By being disciplined, prioritizing timely payments, and avoiding application panic

1min

1min You have just started using credit cards, enjoying the freedom and flexibility they offer.

Good scores = lower rates on home, car, and personal loans.

High scores unlock credit cards with rewards, cashback, and perks.

Good scores = lower rates on home, car, and personal loans.

Good scores = lower rates on home, car, and personal loans.

See How Different Actions Can Affect Your Credit Score Without Impacting Your Real One.

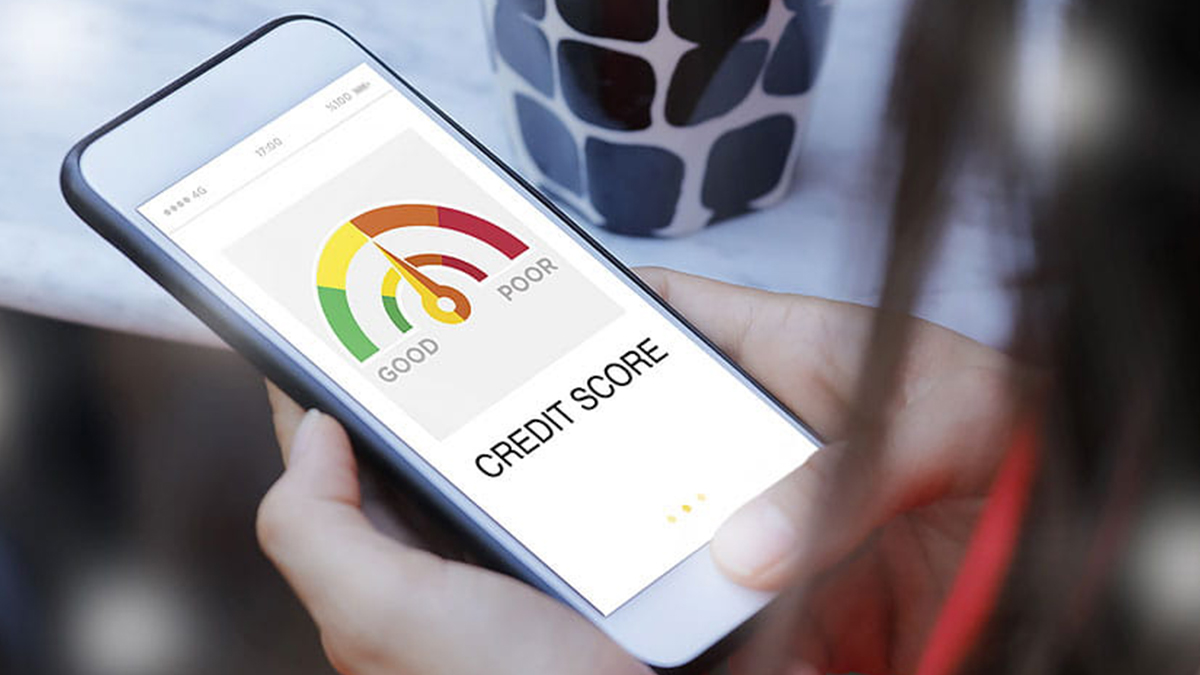

Curious about your Credit Score?

Curious about your Credit Score? See what happens to your score if you apply for or close a loan/credit card, pay off balances or make a late or what happens if you use the full limit on your credit cards

See what happens to your score if you apply for or close a loan/credit card, pay off balances or make a late or what happens if you use the full limit on your credit cardsPowered by

You are being redirected to a third-party website/application (the “Site”) on which YES BANK LIMITED Limited (the “Bank”) exercises no control or ownership. The Bank expressly disclaim any liability for any kind of deficiency in any of the services being provided/facilitated through the Site. The Bank will not be liable or responsible for any kind of loss that you may suffer/incur (i) by availing/relying the Information and/or services being facilitated through the Site, (ii) because of accessing the Site, including but not limited to, any system failure, virus and/or malware attack, data loss, data theft etc., and (iii) due to sharing/disclosing on the Site, any data/information pertaining to you or any third party

Proceed